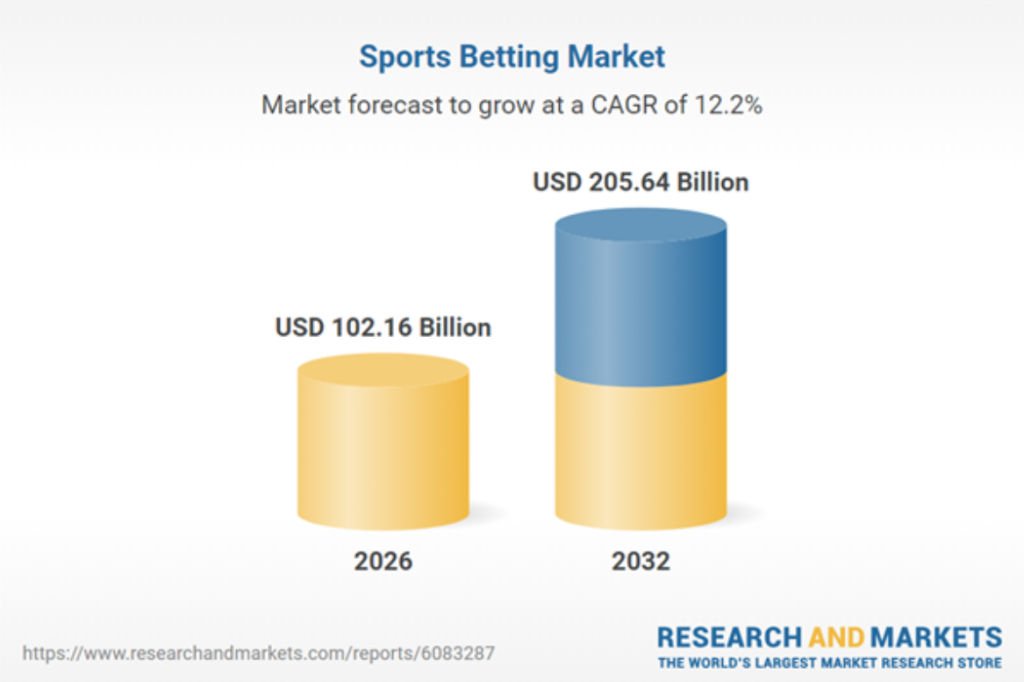

The Sports Betting Market – Global Forecast 2026–2032 report estimated that the market will grow from $91.97 billion in 2025 to $102.16 billion in 2026, before reaching $205.64 billion by 2032. The compound annual growth rate (CAGR) over the period is projected at 12.18 percent.

“The sports betting market in the United States is entering a period of accelerated evolution, shaped by technological innovation, dynamic regulatory landscapes, and changing consumer behaviour,” the report stated. It added that strategic decision-making grounded in robust data and actionable insights has become essential.

Market trajectory and scale

(Source: Research and Markets)

(Source: Research and Markets)

“This exceptional trajectory highlights sustained momentum in both user engagement and revenue expansion, reflecting a convergence of progressive policymaking and rapid technology adoption,” the report said.

The market spans a broad range of bet types, including money line, point spread, parlays, teasers, double chance and totals wagers. Platforms range from casino-based retail sportsbooks to web portals, cloud-based systems and mobile applications on Android and iOS. Engagement takes place across desktop, tablet and smartphone devices, with in-play betting increasingly dominant.

Event categories include pre-match, in-play and virtual sports betting, with synthetic events and esports attracting rising levels of participation. The market also incorporates both mainstream sports such as football, basketball, cricket, tennis and horse racing, and emerging verticals such as competitive gaming.

Payment methods now include bank transfers, debit and credit cards, electronic wallets and cryptocurrency solutions. In the report, the end-user base spans casual bettors to experienced professionals, while geographic analysis covers the Americas, Europe, the Middle East, Africa and Asia-Pacific.

In-play and fast content drive revenue

For operators seeking scalable growth, event frequency and speed are emerging as central revenue drivers. In an exclusive interview with SiGMA News, Chuck Robinson, Chief Revenue Officer at BETER, said that the headline growth figures point to a maturing market. “This projected surge, driven by a 12.18 percent CAGR, confirms that the U.S. market is entering a more mature phase,” he said.

“From our perspective as a global provider, the most scalable revenue driver in this environment is event variety and frequency.”

Robinson argued that while online betting continues to dominate headlines, operators are increasingly responding to demand for immediacy. “While many reports highlight the dominance of online betting, we see a clear shift toward instant gratification. This is where fast-paced content, such as our ESportsBattle series, becomes vital.”

Unlike traditional sports tied to seasonal schedules, fast-cycle content operates continuously. “Unlike seasonal offline sports, 24/7 content directly serves the needs of ‘always-on’ next-generation users, while also acting as the complementary betting content to traditional sports,” Robinson said.

He added that this type of content “helps retain and engage bettors during breaks in live matches (half-time, downtime, mornings, nights, and other off-peak periods), effectively filling gaps in the overall offering.”

The report supports this view, noting that “Virtual and in-play betting are drawing high engagement among younger demographics and are expanding the addressable market beyond traditional retail operations.”

Robinson described in-play wagering as the core engine of future growth. “In-play betting is the engine of this projected $205 billion market, and fast-paced events provide the fuel, minimising downtime and maximising GGR.”

“For operators, this represents the most efficient path to scale: filling the gaps between major leagues with highly engaging, high-frequency content.”

Regulatory divergence and compliance costs

Despite growth prospects, the regulatory environment remains fragmented. The report highlights that “State-level legislation continues to fuel regulatory diversity, demanding flexible compliance strategies and heightened vigilance from operators.”

Robinson said agility depends on three core principles. “First is vendor-led compliance. By working with pre-vetted providers that already hold multi-state authorisations, operators avoid rebuilding systems for every new jurisdiction. This allows them to scale quickly while remaining fully aligned with regulatory requirements.”

The second pillar is technical design. “Second is market-agnostic integration. Core technical infrastructure should be designed to work across jurisdictions, with state-specific rules added as modular layers. This significantly reduces the need for costly system changes and shortens time to market,” Robinson said.

The third is monitoring and integrity. “Third is integrity as a service. Continuous monitoring is essential across all content types. Strong integrity and compliance frameworks help ensure operational continuity, reduce risk, and minimise the need for localised compliance overhead.”

He summarised the approach as a way to “standardise complexity, enabling operators to stay agile, control costs, and focus their resources on growth and acquisition while navigating regulatory fragmentation efficiently.”

The report also noted that responsible gaming mandates are shaping platform design. Tools such as self-exclusion systems and real-time behavioural monitoring are increasingly standard requirements.

Payments and fintech integration

Payments infrastructure is another area undergoing transformation. The report stated that “Operators are leveraging modular service architecture and strategic fintech partnerships to deliver faster settlements and more resilient transaction workflows.”

Robinson said alternative payment methods (APMs) are closely tied to the rise of mobile betting. “The report’s emphasis on online and mobile dominance directly correlates with growing demand for alternative payment methods (APMs). From a provider perspective, this trend is driven by the speed of digital consumption.”

“In a world of fast-paced content and instant bet settlement, players expect ‘instant’ everything. Digital wallets are no longer optional; they are a critical retention tool,” he said, stressing that settlement speed directly affects user retention.

While innovation continues, he cautioned that compliance remains central. “While fintech innovation continues to grow, the priority must remain on seamless, regulated solutions that balance regulatory security with the always-on experience users demand.”

AI, cloud and operational efficiency

Technological investment is another core theme of the forecast. The report highlighted advances “ranging from cloud-based back ends to artificial intelligence, predictive analytics, and mobile-first interfaces” as drivers reshaping user experience.

However, Robinson suggested that the return on investment is clearest in operational rather than marketing applications.

“Today, the strongest ROI is in operational efficiency and risk management. AI is often overhyped; it optimises processes, but it does not solve core business challenges on its own,” he said.

He identified three foundations of measurable returns. “Low latency: Minimal delay is critical for profitable in-play betting, protecting margins, retaining bettors, and enabling efficient scale.”

“Market variety: A broad range of betting markets per event boosts engagement and turnover. Customer personalisation beyond basic segmentation remains overestimated in regulated U.S. markets due to high costs, regulatory constraints, and diminishing returns.”

“Consistency: The availability of content on a 24/7/365 basis, particularly fast-paced formats with multiple simultaneous matches, supports strong bettor presence on operator platforms and ensures constant turnover.”

He added that AI also plays a role in oversight. “Additionally, the use of AI for integrity monitoring creates a scalable environment focused on efficiency and risk management, where ROI becomes measurable, repeatable, and sustainable.”

Tariffs and cost pressures

Beyond technology and regulation, operators are also facing cost pressures linked to international trade measures. The report noted that recent tariff measures affecting imported hardware, software licensing, and data services have increased operational costs for U.S. sports betting operators,” the report noted.

In response, companies are reassessing procurement strategies. “The shift has prompted reexamination of vendor relationships, with nearshoring and local sourcing emerging as practical responses to mitigate expense pressures,” the report said.

Some operators are pursuing internal technology development, while others are adjusting consumer fee structures. These measures, the report states, are influencing “overall industry competitiveness, procurement, and capital allocation priorities.”